didja know that Wisdom Tree launched a CoCo bond ETF last week?

We've discussed liquidity traps before but not in this context.

Markets are made when one entity wishes to sell something and another entity wishes to buy something. If you have something worthless, nobody wants to buy it.

"junk" bonds are those that are risky investments. Because they are risky investments, they earn their holders high interest rates. It's just like car insurance: if you've got a DUI and three accidents on your record, you pay more to insure your car. If you have difficulty paying your credit card bill, your interest rate goes up. The insurance company makes money because the risk of any one driver costing them more than they earn is spread across lots of drivers. This, by the way, is why flood insurance is federally guaranteed: the risk of one homeowner costing more than they earn the insurance company is 100% which means we, the taxpayers, cover the difference.

Nobody is covering the difference in high yield bonds, and there are more high yield bonds right now than ever before.

And when it comes time to sell, there won't be anyone to buy.

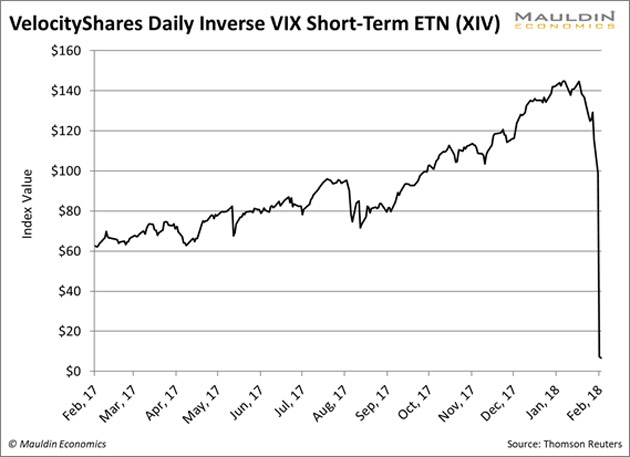

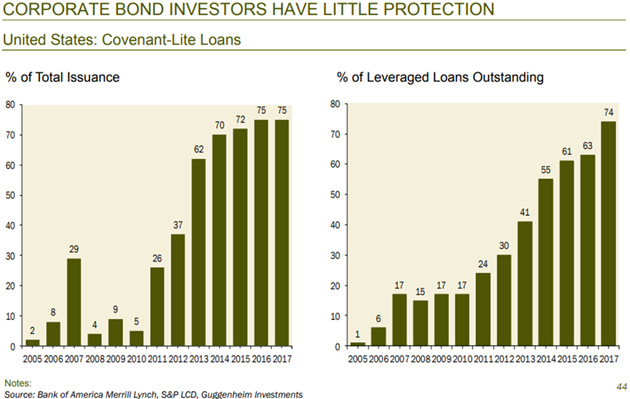

( ^ from the Preview) His parallel of corporate debt being the new mortgage debt is absolutely fascinating. 'Huge if true'. There have been discussions on here before about similar hypotheses, but I feel like this summarizes a bunch of those ideas together. So if I understand it correctly, regular stocks and bonds are no longer yielding enough to keep all our yield-based financial products afloat (e.g. pensions), which has pushed investors into riskier and riskier territory, as that final graph shows and as startup culture (and even crypto?) confirms. If the only things that have a return on investments are Greater Fool Theory-esque things that have little to no real value, it is increasingly likely that we're talking about a row of dominoes easily toppled by one and that I also think there is an interaction effect between corporate debts/spurious VCs, student loan debt/spurious degrees and the erosion of the middle class that is entirely sidelined here. But I don't know enough about any one of those to connect those dots.This time, I believe the collapse will go deeper and happen faster because Dodd-Frank has decimated market makers’ ability to cushion it. Likewise, the Fed will be reluctant to bail out ridiculously priced bonds like WeWork and its many covenant-lite, unsecured brethren

We’re seeing classic end-of-cycle behavior: throw caution to the wind and plunge capital into the market’s riskiest corners. This artificially-induced buying is propping up companies that would otherwise succumb to the fundamental forces arrayed against them.

[...] investors have essentially gone insane.

Had brunch with some friends yesterday. She does benefits for Carnival/Princess Cruises, used to do them for Schwab. He did benefits for Weyerhauser and then Associated Grocers. I was discussing the rise of questionable debt. "So most of these plans were designed to work at a 6% return," I said. "7 to 12%, depending on how optimistic the fund was," she said. "And most of them have been lucky to make 3% since 2000," I said. "3.6% if they were all in cash in 2008. Otherwise 1.7%," she said. "And the Chicago Fed telegaphed last month that we'll be lucky to make 3% for the next ten years," I said. "Well, that I hadn't heard," he said. So. These are the people who, while not directly responsible for the investments, are directly responsible for using the money that comes from those investments. And their figures were more dire than mine. It's one thing if you're trying to make money because you're greedy. It's another thing if you're trying to make money because you fuck over tens of thousands of current and former employees if you can't. Never mind avarice; the bond market is driven largely by obligations and financial structures that collapse if yields aren't made. And funds have no choice when an investment goes south: if the fund has within its bylaws the requirement that all investment instruments must be Moody's AA or above, as soon as one of them drops to B they have to sell it. They are compelled by law to sell it. No one is compelled by law to buy it. So they sell it at a steep loss and now they have to invest in something else. And it must be Moody's AA or above. And they were likely not the only fund in that instrument so they're not the only ones dumping garbage and trying to buy sterling. Repeat times every local, municipal, national, corporate, private and educational equity firm. Mauldin is pretty good about completely ignoring that which does not have his attention at the moment.I also think there is an interaction effect between corporate debts/spurious VCs, student loan debt/spurious degrees and the erosion of the middle class that is entirely sidelined here.

Holy shit. I'm a huge believer in coworking spaces, have actively used and promoted them, and have been a member of - and know people who currently are members at - WeWork. I had never heard of SPE's, though. That some crafty financial skullduggery, right there. And a wicked-rickety tower to stand $20bn of valuation on top of! I still like the Office Nomads model: Own the building. Full disclosure: I was a tenant for several years, and am personal friends with the owners.

This is the first I've heard of the coworking movement--it reminds me a bit of the hacker/maker-space trend. It seems robust in theory, but I can see the execution being tricky. I would think that owning the space is the safest, though not the easiest, way to go about establishing one of these spaces.

Coworking is freaking magical for the solopreneur. Sitting at home on your couch typing on a laptop is only going to get you to about $2k/month, if you REALLY work at it. There's only so much money people will pay someone, when their office is a coffee shop. In a coworking space, the energy and vibe of the space just makes money fall outta the sky. Think of it: If you work for yourself, and you don't want to work today, you don't go in to the coworking space and faff about on Facebook, or go into YouTube spirals. Instead, you stay home, or go to a coffee shop. So a coworking space FEELS different... the air is spicy with energy and productivity. People are there because they are WORKING. When the productivity stops, they leave. Being in that kind of electrically-productive environment stimulates the brain cells, and makes you hyper-productive. AND, it gives you an office where you have a conference room, and a secretary, and a printer, and you can meet clients and do presentations, and brainstorm on whiteboards. You can't do that in a coffee shop. Coworking is brilliant. Took my business from about $1000-$1500/month to more than $5k/month. Made ME better. More confident. More professional. More productive. I'm a fan. Can you tell? =>

"One top San Francisco broker put it this way, 'WeWork’s openly been saying for years that if the market tanks, it’ll renegotiate every lease it has.'"It may be that WeWork will shiv its landlords only when it becomes truly desperate, but with $18 billion in short and medium-term debt and losses running nearly a billion a year, desperation may arrive sooner than anticipated. This, by the way, is where WeWork’s pivot to the Fortune 500 is going to bite harder than a third grader in a schoolyard fight. Sublease 100,000 feet to 400 dinky entrepreneurs and start-ups and chances are some will prove to be cockroaches that survive the next downturn—the space may stay half-leased. Sublease that same 100,000 feet to General Motors or Microsoft, companies with better—and more conservative—economic forecasting models than you’ve ever dreamed of, and they will go dark before your feet hit the floor.